Frequently asked questions

Does the premium come to my practice?

No. Premiums are paid to the insurance company. Your practice is paid through the client's copay/coinsurance plus the insurer's reimbursement.

Why do clients owe more in January?

Most deductibles reset at the start of the calendar year, so clients pay more out of pocket until they meet it again. Flagging this in December saves a lot of confusion.

Want help setting up systems that make benefits conversations easy for your team?

Book a free consultation or explore my other free tools.

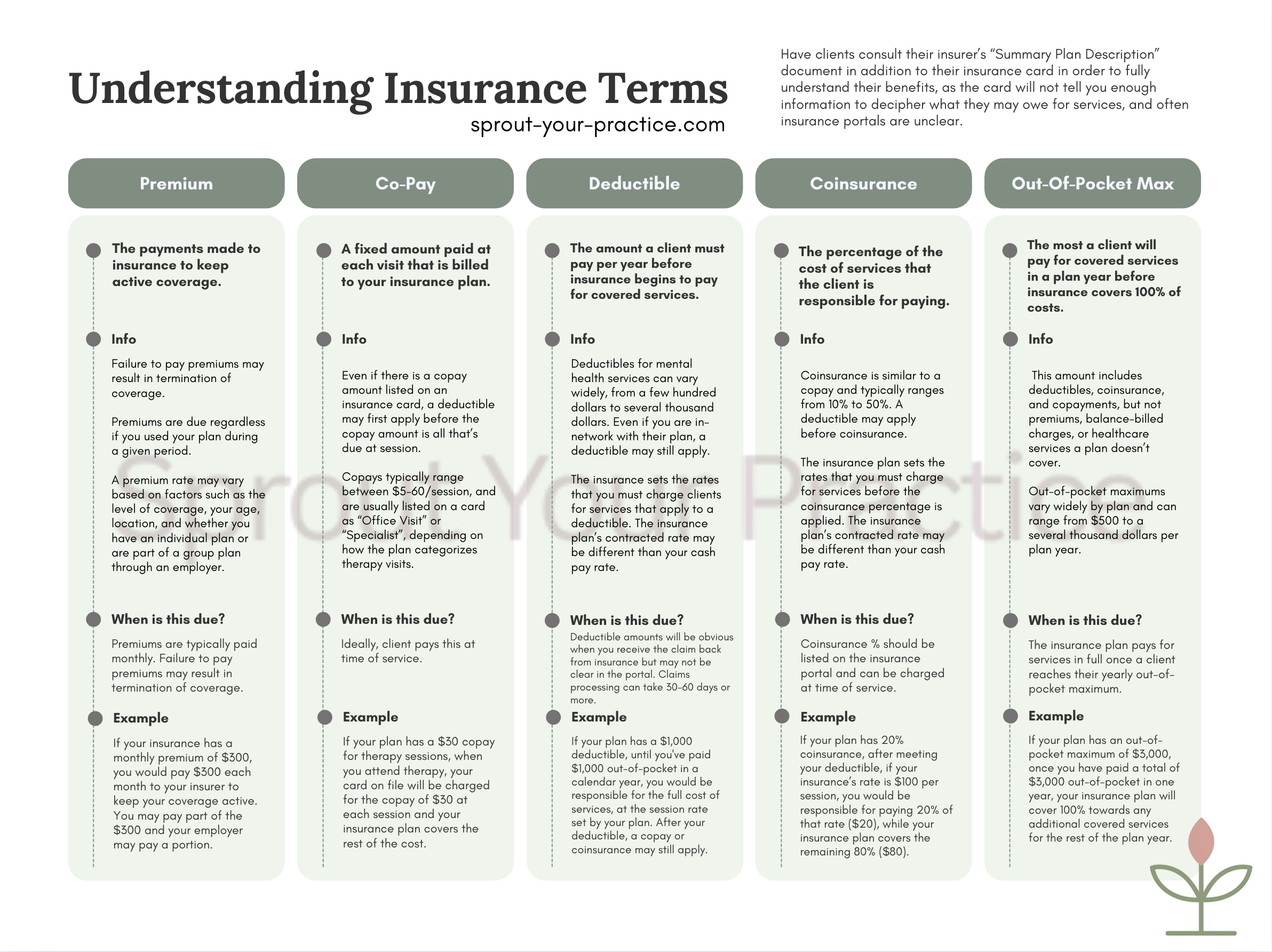

Insurance Terms Every Therapist Should Know

If insurance language makes your eyes glaze over, you're in good company. When I started Sprout Therapy PDX, I learned these terms the hard way — usually while trying to explain a surprise bill to a client. Here's the short version: a premium is what someone pays to have insurance, a deductible is what they pay before insurance chips in, and a copay or coinsurance is their share of each visit after that. Below, I break down each one in plain English so you can talk about coverage with confidence.

Why these terms matter for your practice

You don't need to become a billing expert, but you do need enough fluency to set expectations. Clients who understand their benefits are less likely to be blindsided by a bill — and less likely to drop out of care because of one. Clear communication here is part of ethical, client-centered practice, not just admin.

What is a premium?

The premium is the amount your client pays — usually monthly — just to have the insurance plan, whether or not they use it. Think of it like a gym membership: you pay it to keep access, separate from what any single visit costs. Premiums don't come to your practice; they go to the insurer.

What is a deductible?

The deductible is the amount a client pays out of pocket each year before their insurance starts paying for services. If someone has a $2,000 deductible, they typically cover the full negotiated rate of their sessions until they've spent $2,000 — then their plan kicks in. This is the term that surprises clients most, especially early in the calendar year when deductibles reset.

What is a copay?

A copay is a fixed dollar amount the client pays per visit — say, $30 a session — regardless of the total cost. Copays often apply even before the deductible is met, depending on the plan. They're predictable, which clients appreciate.

What is coinsurance?

Coinsurance is a percentage of the session cost the client pays after they've met their deductible. If their coinsurance is 20%, and the allowed rate for a session is $150, they pay $30 and insurance pays the rest. Unlike a copay, it moves with the cost of the service.

What is an out-of-pocket maximum?

This is the safety net. Once a client has paid a set amount in a year (through deductible, copays, and coinsurance), their plan covers 100% of covered services for the rest of the year. Premiums don't count toward this maximum.

How they fit together: a quick example

Say a client has a $1,500 deductible, 20% coinsurance, and a $4,000 out-of-pocket max. For their first sessions, they pay the full allowed rate until they hit $1,500. After that, they pay 20% per session. If their year gets expensive and they reach $4,000 total, everything covered is free for the rest of the year. Same client, three different costs — depending on where they are in the year.

Start Your Practice with Clarity

Sign up below to get my free Practice Vision & Values Worksheet — the first step to building a sustainable, ethical practice.

You’ll also get occasional practice-building tips and tools! No spam, just resources I wish I had starting out.